The Affordable Care Act (ACA) led to historic gains in health insurance coverage by extending Medicaid coverage to many low-income individuals and providing Marketplace subsidies for individuals below 400% of poverty. Under the law, the number of uninsured nonelderly Americans decreased from 44 million in 2013 (the year before the major coverage provisions went into effect) to less than 28 million as of the end of 2016. Recent efforts to alter the ACA or fundamentally change the structure of Medicaid may pose a challenge to further reducing the number of uninsured and may threaten coverage gains seen in recent years.

The questions below describe how coverage has changed under the ACA, examines the characteristics of the uninsured population, and summarizes the access and financial implications of not having coverage.

Why do people remain uninsured?

Even under the ACA, many uninsured people cite the high cost of insurance as the main reason they lack coverage. In 2016, 45% of uninsured adults said that they remained uninsured because the cost of coverage was too high. Many people do not have access to coverage through a job, and some people, particularly poor adults in states that did not expand Medicaid, remain ineligible for financial assistance for coverage. Some people who are eligible for financial assistance under the ACA may not know they can get help, and undocumented immigrants are ineligible for Medicaid or Marketplace coverage.

Who remains uninsured?

Most uninsured people are in low-income families and have at least one worker in the family. Reflecting the more limited availability of public coverage in some states, adults are more likely to be uninsured than children. People of color are at higher risk of being uninsured than non-Hispanic Whites.

How does the lack of insurance affect access to health care?

People without insurance coverage have worse access to care than people who are insured. One in five uninsured adults in 2016 went without needed medical care due to cost. Studies repeatedly demonstrate that the uninsured are less likely than those with insurance to receive preventive care and services for major health conditions and chronic diseases.

What are the financial implications of lacking coverage?

The uninsured population often face unaffordable medical bills when they do seek care. In 2016, uninsured nonelderly adults were over twice as likely than their insured counterparts to have had problems paying medical bills in the past 12 months. These bills can quickly translate into medical debt since most of the uninsured have low or moderate incomes and have little, if any, savings.

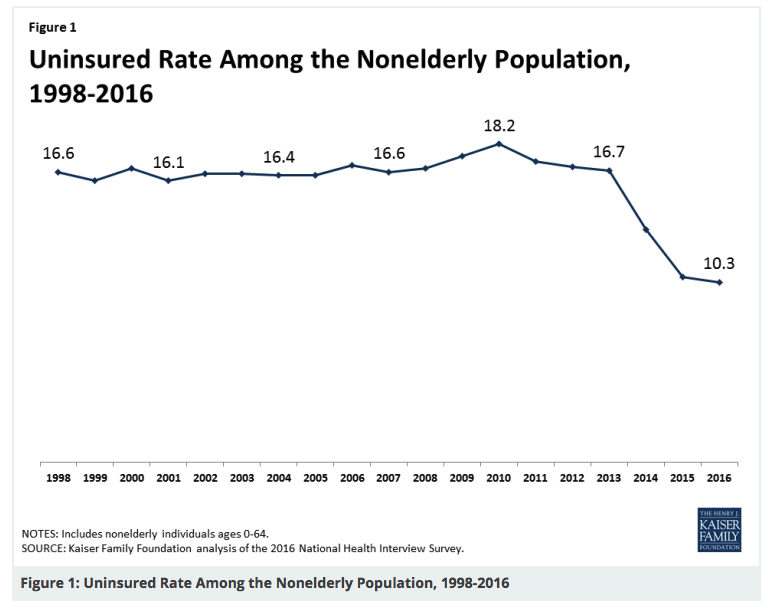

How has the uninsured population number changed under the ACA?

In the past, gaps in the public insurance system and lack of access to affordable private coverage left millions without health insurance, and the number of uninsured Americans grew over time, particularly during periods of economic downturns. By 2013, more than 44 million people lacked coverage. Under the ACA, as of 2014, Medicaid coverage has been expanded to nearly all adults with incomes at or below 138% of poverty in states that have expanded their programs, and tax credits are available for people who purchase coverage through a health insurance marketplace. Millions of people have enrolled in these new coverage options, and the uninsured rate has dropped to a historic low. Coverage gains were particularly large among low-income adults living in states that expanded Medicaid. Still, millions of people—27.6 million nonelderly individuals in 2016—remain without coverage.

- Coverage gains from 2013 to 2016 were particularly large among groups targeted by the ACA, including adults and poor and low-income individuals. The uninsured rate among nonelderly adults, who are more likely than children to be uninsured, dropped from 20.5% in 2013 to 12.2% in 2016, a 40% decline. In addition, between 2013 and 2016, the uninsured rate declined substantially for poor and near-poor nonelderly individuals (Figure 2). People of color, who had higher uninsured rates than non-Hispanic Whites prior to 2014, had larger coverage gains than non-Hispanic Whites. Though uninsured rates dropped across all states, they dropped more in states that chose to expand Medicaid, decreasing by 7.1 percentage points compared to 3.7 points in non-expansion states.

For more statistics and facts about the uninsured population in the United States visit Kaiser Family Foundation.